Investment Results

This web page provides a discussion of my portfolio performance for the reporting period ended Friday, July 1, 2011. My objectives are wealth accumulation in real terms, sufficient to meet Beverly and my's desired standard of living. The table below shows the most recent investment performance against my benchmark portfolio, which is composed of 30% allocated to the MSCI World Index & 70% allocated to Aggregate Bonds. This benchmark started July 2010. Prior to July the benchmark was 100% MSCI World Index. The change in benchmark reflects a change in strategy focused on acceptable levels of volatility for our planning horizon.

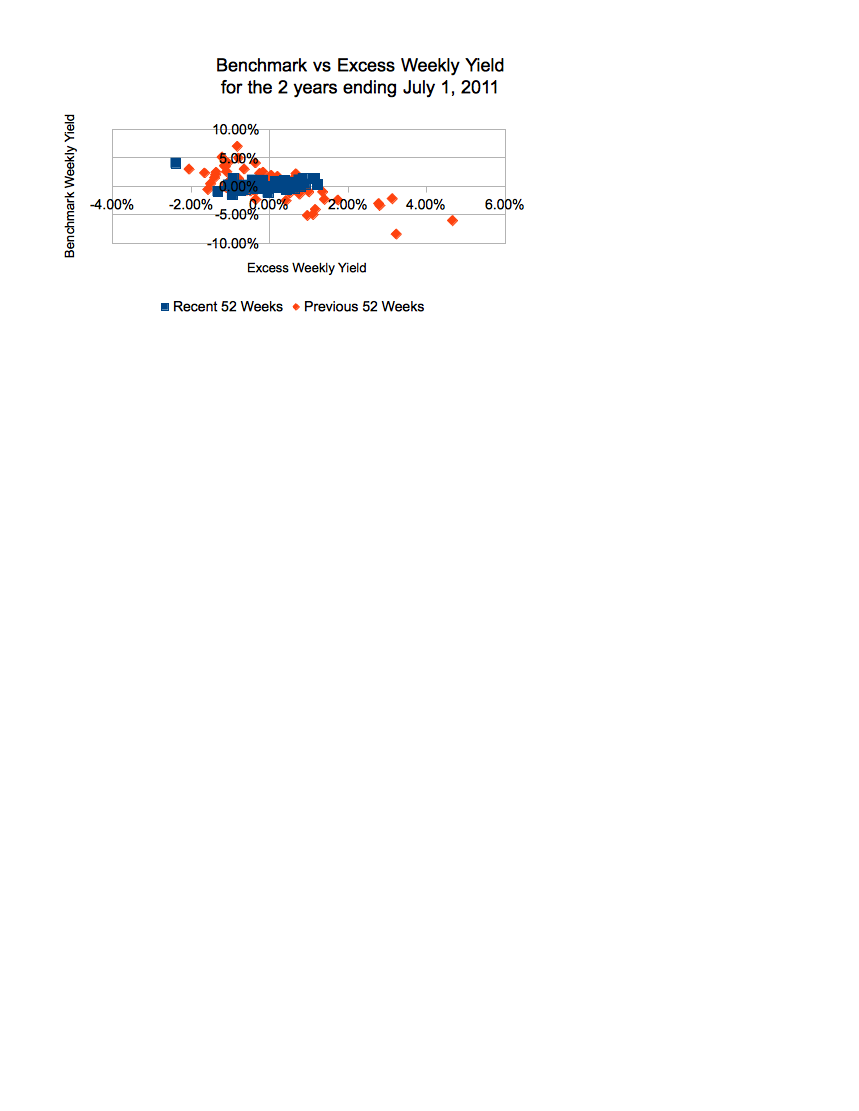

I have underperformed the primary benchmark for the 6 month, and 1 year timeframes and outperformed on the 2 year time frames, as indicated by the positive monthly average excess yields (alpha). Primary benchmark performance has come at a reasonable risk reward as indicated by the information ratio at or above the average performance of the average mutual funds for all time frames.

My performance in indicative of keeping pace with the desired benchmark. As my asset allocation places a larger weight on equity, some might point to an underperformance of the equity investments and suggest a change in asset class weighting. However, giving my low portfolio turnover objective, providing more time for the allocation to meet expectations is consistent with strategy.

| Investment Performance Against Benchmark | |||

|---|---|---|---|

| Periods Ended July 1, 2011 | |||

| Annualized Returns | |||

| 6 months | 1 Year | 2 Years | |

| Personal Portfolio | 1.2% | 7.9% | 11.5% |

| Benchmark Assets | 4.0% | 11.2% | 10.4% |

| Average Weekly Excess Yield Against | |||

| 6 months | 1 Year | 2 Years | |

| Benchmark Assets | -0.05% | -0.06% | 0.01% |

| Information Ratio | |||

| 6 months | 1 Year | 2 Years | |

| Benchmark Assets | -0.0828 | -0.0856 | 0.0090 |

| Average Mutual Fund | -0.0840 | ||

| Top 25% of Mutual Funds | 0.0600 | ||

| World Class Performance | 0.50 + | ||

Investment Environment

As we begin July 2011, the global economy is forecast to grow, yet new debt fears in Europe have caused turmoil in the markets. And we may be in the beginning of debt fears of the US. The US Treasury department projects, a default by the US government if the debt ceiling is not raised by the US Congress by August 2. The political games are in full progress, with unpredictable results for those trying to attain political gains. The next few months can see extreme volatality, for me it is watch and wait. Profits and cash positions at multinational corporations appear strong, however, worker wages, in the US at least, are stagnant. It is becoming increasingly clear that the US economic growth will be lower than the world average, as debt fueled spending ends. However, the US Dollar appears to still be the currency of choice as a safe haven. Thus, the US enjoys low interest rates when its economic performance, otherwise would not warrant investor cooperation. With my increased concern that the rest of the world, and profit hungry US traders, will catch on to this unintended benefit for US consumers, I've moved money out of US inflation protection and into global inflation protection. The results of the current debt ceiling negotiations may yet support the wisdom of this move.

China and Brazil in particular appear poised for growth in their internal economies. Both are characterized with the potential for expansion in the middle class ranks, without having heavy debt loads. This is the opposite of the United States, which has a large debt load, and a shrinking middle class ranks. Global pressures for inflation show up in these countries and their Central Banks are having to temper growth to avoid high inflation and rising currency. However, it will take time for central banks to come and understand a declining US Dollar, appreciation in their own currencies, and the resulting effect on middle-class growth. Inevitably, I expect, the central banks will get it figured out, and remove restrictive policies against currency appreciation. This will make for a slow and steady depreciation of the USD against specific currencies.

My key hypothesis summarized:

- World economic growth is greater than US economic growth, and generally low than historically occurrences

- Deflation of the US currency relative to the rest of the world occurs

- Growth in commodity exports and employment stabilization as world economies transition away from using leverage and financial services to generating profits through other means.

- Global financial institutions will move capital to the most productive places, which can be recognized by:

- low real wages and excess workers

- relatively high interest rates with an macro economic environment to support a downward trend

- intellectual capacity to turn innovation into profits or exports

I will carefully keep an eye on the US push to develop clean energy as a industry specialization. Profit opportunities could exist here, but a little too early to make concerted investments. With the November result on Prop 23 in California, the opportunity for clean energy expansion increases. Outside the US the interest is to find countries with a recipe for expanding capital investment. They will have the double benefit of borrowing in USD (with expectations for a declining dollar) while receiving foreign direct investment and experiencing next exports. As a result, real growth and currency increases against the USD provide a formula for high investment returns.

Additionally an excellent read is The Growth Report published by the Commission on Growth and Development. There are good ideas that can help you find investment opportunities.

Click here to read The Growth Report

Click here to read the World Economic Outlook, April 2010

Information Ratio Interpretation

I monitor investment results, not only to keep myself honest, but to remind myself to never loose focus on using my talents to the benefit of my household. By using the information ratio to measure investment performance, my challenge becomes to produce high excess returns relative to the risk taken. This is a good honest challenge. Reilly & Brown discussed in Investment Analysis Portfolio Management pg 1123, an empirical study which was performed on 20 Mutual Funds evaluating the information ratio score of the portfolio managers. For the 20 Select Mutual Funds, the mean IR was -0.0840 and the median IR was -0.0680. This study helped support the now well established notion that the average mutual fund manger does not out perform benchmark indexes. The top 25% of mutual funds in the study (5 funds) reported an IR of 0.0600. Well at least the top 25% had positive excess returns.

In 1995, Grinold & Kahn wrote an article in Active Portfolio Management where they proposed a standard for professional portfolio mangers as follows:

- # Good >= 0.5000

- # Exceptional >= 1.0000

Portfolio Composition as of July 1, 2011

- EWZ - 32.3%

- WIP - 18.8%

- EWS - 8.1%

- PTTAX - 20.6%

- LQD - 17.8%

- Cash - 2.4%

Recent Video

I watched this video and was impressed with how the Stanford thinking still filters through my mind. I found myself agreeing with many aspects of the discussion, and more confident that my long term investment view will be realized. The discussion on inflation risk for this country is illustrative. The explanations offered for the simplicity of CDS (Credit Default Swaps) and complexity of CDO (Collateralized Debt Obligations) are informative. Hope you enjoy the video as well.

Places Visited

September 2010

Beverly and I made our normal journey to Northern California for Labor Day. The visit was wonderful. No special activities, and the city seemed a bit quite but, the company, restaurants, and drink were outstanding. I promised pictures, previously, but alas, most are pictures of family so they are not posted. I did discover TRX training on this trip, interesting concept. My intended Christmas gift for myself. And by December, I'll need a change of pace for my exercise program.

December 2009

Beverly and I traveled to Bahia to spend Christmas and New Years with our friends. The two families meet in Praia do Forte and we had one of the best vacations. Best, not because of the exciting and famous things we did, but because we were able to relax, release the tensions of everyday life, and enjoy life. We spent the days near the pool or beach, home cooked meals for lunch, and pleasant dinners out and about in Praia do Forte. We took a day trip to Salvador, which was wonderful. I think I will have to return to Salvador again. Too much to experience in just one day. Based on our one day, visit, it is extremely clear, retail spending is on a boom in Salvador. I saw it. My friends who live in the South, of Brazil, saw it. The lines, the activity, the number of people with bags in their hands.

Pictures are posted at my new website hosted by zenfolio.

Click here to see my photo collection

September 2009

Beverly and I traveled to Northern California for the Labor Day weekend. As with the previous year we visited Beverly's god sister & husband, and my good friend from graduate school. As always there was plenty of good food and drink, and the company was outstanding. We got a chance to visit Sausalito for the Art festival. The crowd was excited for all the bands and the scenery was spectacular. While I carried my camera plenty of places, somehow I wasn't in the photo taking mood. Sorry about that. Next time, there will be pictures.

May 2009

Beverly and I shared a wonderful Mother's Day weekend as the guest of dear friends in Miami. The event was called a Celebration of Friendship. A more than appropriate descriptor. I had never really been to Miami so the visit was a learning experience for me. Not that we saw all there was to see, but the small bit I did see was very nice. Of course staying at a Ritz Carleton never hurts in developing a nice impression of anything.

I was most impressed with the warm sense of belonging that comes over you when you reconnect with someone you did not realize you missed. Just as the smell of freshly baked goods tends to recall very specific memories, I'll now have a marker in my mind for Miami. Will Smith put one marker in my mind with his song Miami, but this weekend provides another. Just maybe this marks a transition in life.

Books Read

My recently read books include:

- Silver Sparrow by Tayari Jones

- Why Some Things Should Not Be for Sale by Debra Satz

- Before You Suffocate Your Own Fool Self by Danielle Evans

- At the Jazz Band Ball by Nat Hentoff

- Poemcrazy by Susan G. Wooldridge

- This Year You Write Your Novel by Walter Mosley

- Leaving Atlanta by Tayari Jones

- Architects of Poverty by Moeletsi Mbeki

- The Art of Changing The Brain by James E. Zull

- Thabo Mbeki and the Battle for the Soul of the ANC by William Mervin Gumede

Danielle Evans, suggested by Tayari Jones, was excellent. A series of short stories about the lives of less than perfect young people dealing with the joy, confusion, and pain of life. I found the stories a wonderful escape from my own life, insightful yet rewarding to read and reflect. I'd think a plus for reading and discussing among friends.

Tayari Jones' books are very enjoyable. I found myself immersed not only in the story, but also remembering my own life events. And that is a meaningful tribute to this author. I heartily recommend both Leaving Atlanta and Silver Sparrow, as I myself look forward to future work from Tayari. For Twitter fans, Tayari can be found at:

Moelestsi Mbeki's book, in many ways a good follow up to William Gumede's book, explores not only the problems with developing a democratic society that serves the people broadly, but many solutions. I applaud his effort, however I can only hesitate to determine if others will follow some sibilance of this suggestions. Not that I see his suggestions as a golden path, but the underlying values supporting the suggestions appear, in my view, rock solid. Thus following the values may lead to different recommendations, but in the end a growing middle class would result. For investors in any growing democracy there are important lessons and judgments exposed.

James Zull's book was fascinating and very stimulating. I've put many of the ideas into practice with my godchildren and protege. An important read for anyone interested in helping others learn and develop.

William Gumede has written an enlightening book on the ANC and the very being of South African politics. I found it enjoyable, and every bit as thorough as The Brazilians was to Brazil. A good read, and if you are considering investing in South Africa, this is the definitive primer.